Understanding the Earned Income Tax Credit (EITC)

Discover the valuable assistance offered by the Earned Income Tax Credit (EITC) for individuals and families with modest incomes. Learn about eligibility requirements, income limits, and how the cr...

Evangeline Giron and Tatianna Giron

1/10/20242 min read

Understanding the Earned Income Tax Credit

The Earned Income Tax Credit (EITC) is a tax benefit designed to assist low to moderate-income individuals and families. It is intended to provide financial support and help alleviate the burden of taxes for those who are working but earning modest wages. The credit is refundable, meaning that if the credit exceeds the amount of tax owed, the taxpayer may receive the excess as a refund.

Eligibility and Income Limits

To qualify for the EITC, there are specific eligibility requirements that need to be met. Firstly, the taxpayer must have earned income from employment or self-employment. Earned income includes wages, salaries, tips, and self-employment income reported on a W-2 or a Schedule C.

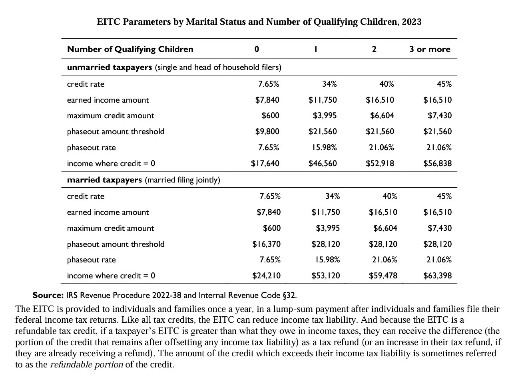

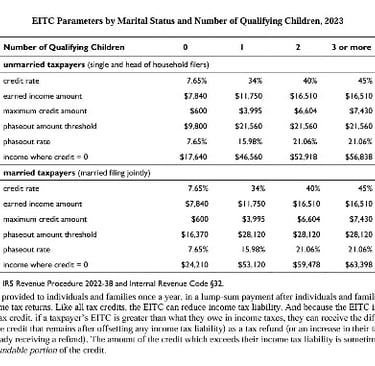

Additionally, there are income limits that determine the maximum amount of EITC a taxpayer can receive. These limits are based on the taxpayer's filing status and the number of qualifying children they have. The maximum number of qualifying children per tax return is three.

Calculating the EITC and Adjusted Gross Income (AGI)

The amount of EITC a taxpayer can claim is based on their earned income and the number of qualifying children. However, it's important to note that the overall Adjusted Gross Income (AGI) is used in the income criteria. AGI includes not only the earned income but also other sources of income such as investment gains, Schedule K-1 from LLC or corporations, gambling winnings, and unemployment benefits.

Let's consider an example to illustrate how the EITC is calculated based on AGI. Suppose a taxpayer has a W-2 income of $15,000 and investment income of $5,000. In this case, their AGI would be $20,000. The EITC would be determined based on this AGI amount.

However, if the taxpayer's income consists solely of unemployment benefits and investment income, both totaling $20,000, they would not qualify for the EITC. This is because unemployment benefits and other income sources, apart from earned income, are not considered eligible for the EITC.

In conclusion, the Earned Income Tax Credit provides valuable financial support to individuals and families with modest incomes. It is essential to understand the eligibility requirements, income limits, and the calculation of the EITC based on Adjusted Gross Income. By claiming this credit, eligible taxpayers can reduce their tax liability or receive a refund, helping to improve their financial situation.

T

©Copyright 2024: Fiscal Foundations 101 All rights reserved

tax@evangelinegiron.com